Understanding your Taxes

Here we are again. It is tax season for most filers. If you are not sure how to make heads or tails of your tax return, or if you are curious about how tax planning changes from wealth accumulation to retirement, keep reading!

Your federal 1040 tells a financial story about you and your household. But before we get into the specifics, if you aren’t perfectly clear on the story being told, you are not alone. According to the National Taxpayer Advocate, an independent organization within the IRS, in their annual report to Congress, has identified taxpayer confusion and frustration with tax laws and forms as a significant issue. (You probably already know this!) Your Congress people absolutely know this.

- A substantial percentage of users feel overwhelmed by the tax preparation process and are unsure if they’re maximizing their deductions and credits

- Many taxpayers struggle with basic tax concepts, such as determining filing status, understanding deductions and credits, and completing forms accurately

Even though tax confusion reigns, IRS data reports the overall error rate for individual income tax returns has been relatively low in recent years. For example, in the IRS Data Book for the fiscal year 2020, the IRS reported an overall error rate of 1.80% for individual income tax returns filed for the tax year 2019.

The 7 “Chapters” of a Tax Return

Your 1040 tells a story about your financial situation and tax obligation for a particular tax year. The story is told through the following:

- Income Sources: The 1040 return provides details about the various sources of income that the individual or couple (MFJ) received during the tax year. This may include wages or salary, self-employment income, interest and dividends, capital gains, rental income, retirement income, and other forms of income. (Please note there are other ways to file: Head of Household, Married Filing Separately and Qualifying Widow(er) with Dependent Child).

- The return shows deductions that the individual/couple is eligible to claim, which can reduce their taxable income. Common deductions include those for mortgage interest, property taxes, medical expenses, charitable contributions, student loan interest, and certain business expenses.

- Credits: Tax credits directly reduce the amount of tax owed and can be refundable or non-refundable. The tax return indicates any credits the individual qualifies for, such as the Earned Income Tax Credit, Child Tax Credit, Education Credits, and various other credits available based on specific circumstances.

- Taxable Income: After accounting for deductions and credits, the tax return calculates the individual’s taxable income, which is the amount on which they owe taxes.

- Tax Liability: The tax return shows the individual’s total tax liability, which is the amount of tax they owe to the government based on their taxable income and the applicable tax rates.

- Tax Payments and Refunds: The tax return indicates any tax payments the individual has already made throughout the year, such as through withholding from wages or estimated tax payments. It also shows whether the individual is entitled to a refund or if they still owe additional taxes.

- Compliance: By filing a tax return, the individual is complying with their legal obligation to report their income and pay taxes according to the tax laws. The accuracy and completeness of the information provided on the tax return reflect the individual’s commitment to complying with tax regulations.

Sounds pretty straightforward, right? How you plan is dependent upon your stage of life. In this article we explore the accumulator stage and the de-cumulator stage (the retiree).

Differences in Tax Planning for the Accumulator vs. the Retiree

Tax planning for a retiree and a wealth accumulator can differ significantly due to variations in income sources, tax obligations, retirement accounts, and overall financial goals. Generally, accumulators are looking for ways to defer taxes, while a retiree may be trying to balance income generation and tax obligations. Here are some key differences in tax planning considerations for retirees versus accumulators:

| Category | Accumulators | Retiree |

|---|---|---|

| Income Sources | typically derive their income primarily from wages or salary earned through employment. They may also have investment income, such as dividends or capital gains, but it may not be as significant as their earned income | often has multiple sources of income: retirement account distributions (such as 401(k) or IRA withdrawals), Social Security benefits, pension payments, annuities, investment income, rental income, and possibly part-time employment income. |

| Retirement Accounts | may be actively contributing to retirement accounts such as 401(k) plans, IRAs, or Roth IRAs, and they may focus on maximizing contributions to these accounts to benefit from tax-deferred growth or tax-free withdrawals in retirement. | may have accumulated funds in tax-deferred retirement accounts (such as Traditional IRAs or 401(k) plans), Roth IRAs, and taxable brokerage accounts. Withdrawals from traditional retirement accounts are generally taxable as ordinary income, while qualified withdrawals from Roth IRAs are tax-free. |

| RMDs (Required Minimum Distributions) | may be actively contributing to retirement accounts such as 401(k) plans, IRAs, or Roth IRAs, and they may focus on maximizing contributions to these accounts to benefit from tax-deferred growth or tax-free withdrawals in retirement. | Those who have reached age 73 are generally required to take annual withdrawals, (RMDs), from their tax-deferred retirement accounts. These distributions are subject to income tax. |

| Tax Strategies | may focus on tax-efficient investing strategies, such as investing in tax-advantaged accounts, harvesting tax losses to offset gains, and maximizing deductions for expenses related to education, home ownership, or healthcare. | may employ tax strategies to minimize taxes on their retirement income, such as managing the timing and size of withdrawals from retirement accounts, taking advantage of tax deductions for medical expenses or charitable contributions, and considering the tax implications of Social Security benefits. |

| Long Term Planning | may focus on long-term tax planning strategies that align with their financial goals, such as saving for retirement, funding education expenses, or purchasing a home. | may need to plan for the tax implications of their estate and inheritance for their beneficiaries. They may also consider strategies to minimize taxes on their retirement savings while ensuring they have sufficient income for their retirement years. |

The Accumulators

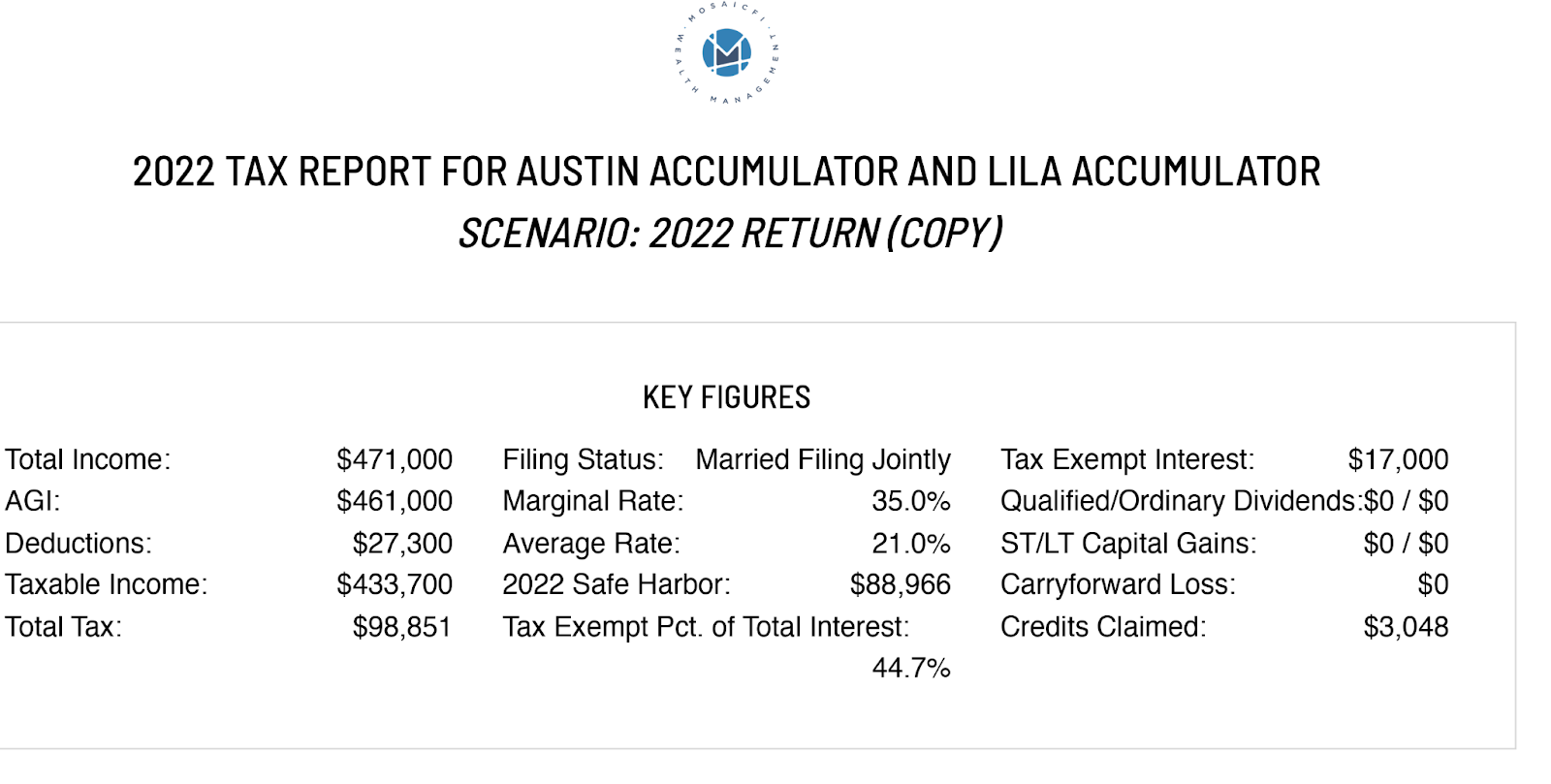

Let’s take a peek at two examples. Our accumulators are Austin & Lila. Here is a snapshot of their financial situation:

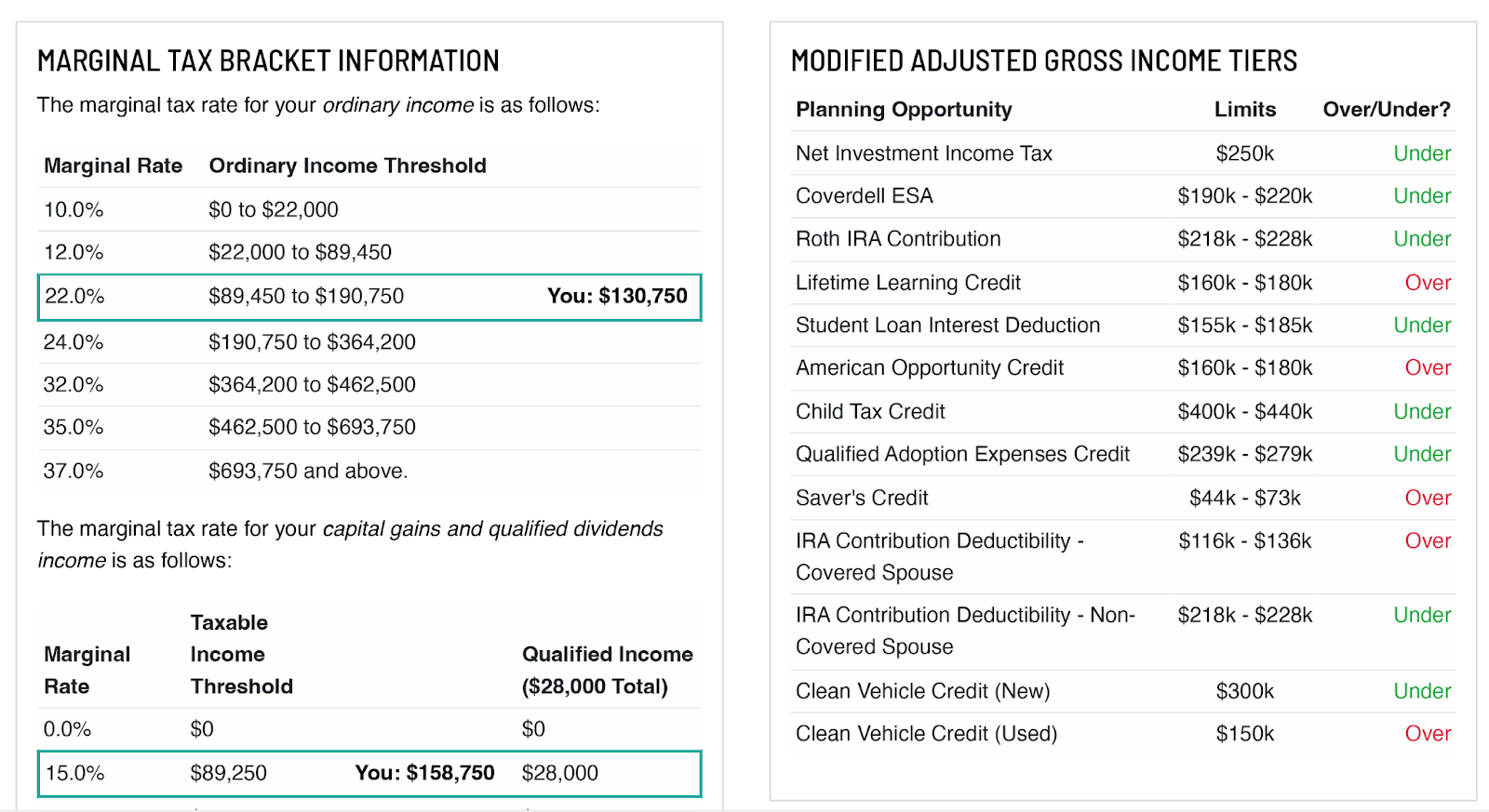

Together, Austin & Lila earn a high income.

As you can see, their marginal tax rate is 35% and their effective or average tax rate is 21%.

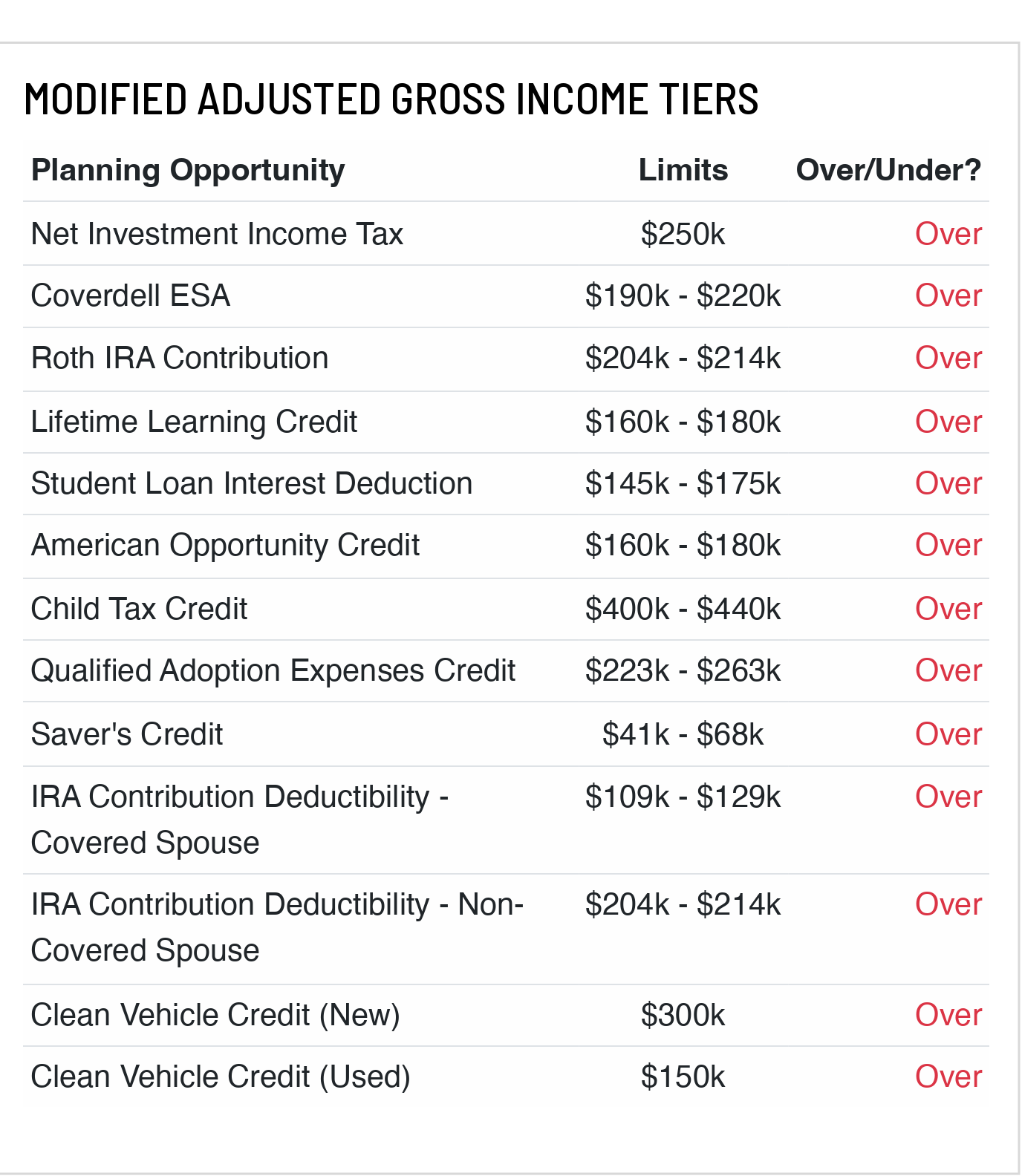

With regard to planning opportunities, because of their high income, they are over the thresholds in the categories above.

While they earn too much for a Roth IRA Contribution, they may be able to do a Backdoor Roth strategy.

In addition, their income exceeds the threshold for the 3.8% Net Investment Income Tax (NIIT). They may want to consider strategies like investing in municipal bonds or making charitable donations to reduce taxable income and be mindful of realized capital gains.

Something else to consider is making sure they are taking full advantage of pre-tax options in their respective employer-provided benefits.

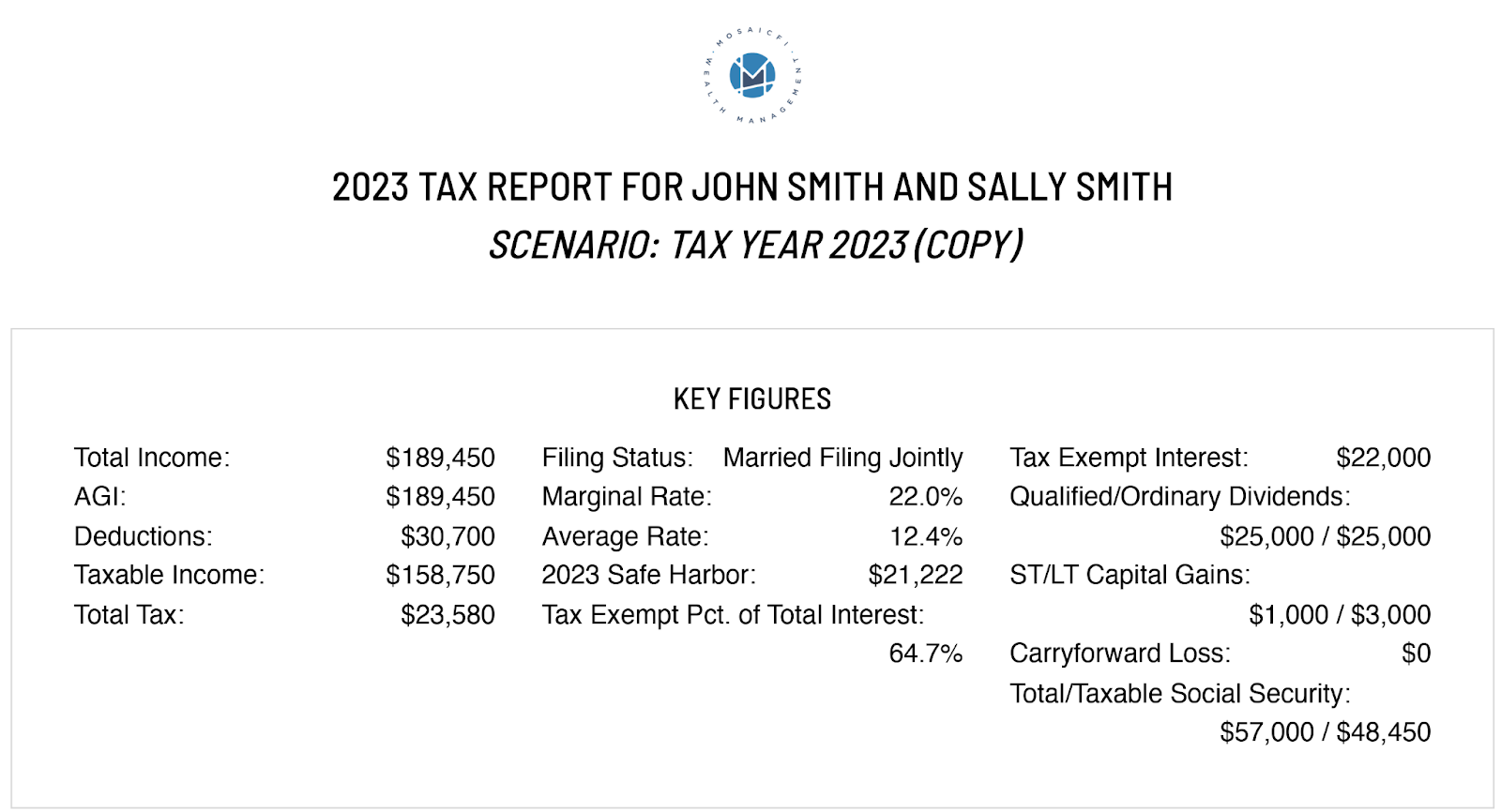

Now, let’s look at a Retiree couple, John and Sally.

The Retirees

John and Sally Smith derive their income from multiple sources including Social Security, RMDs, Capital Gains and Dividends and Interest.

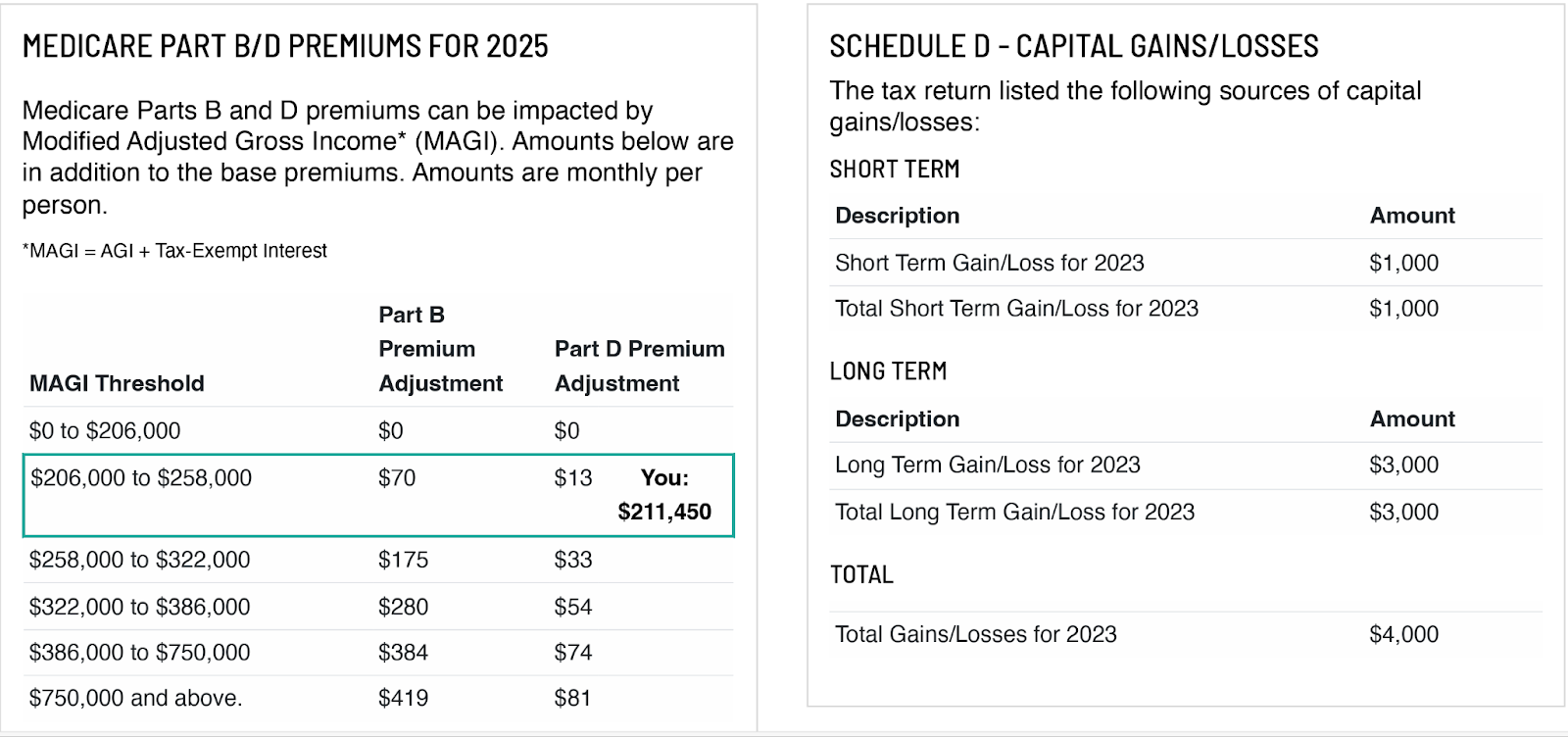

They are in the 22% marginal tax bracket and their effective/average rate is 12.4%. For retirees, those 65 and older, another important set of numbers to pay attention to includes the following schedule which determines the amount of their Medicare Premium for Part B/D.

The premium is determined by the MAGI (modified adjusted gross income) which is the AGI plus tax-exempt interest. In this case, John and Sally have a MAGI of $211,450, which puts them in the next lowest bracket for their monthly per person premium. For 2024 the lowest Medicare Premium is $174.40, the next lowest is $244.60. John and Sally will pay a total of $489.20 per month for their Medicare rather than $348.80. This may be a planning opportunity.

Like the Smiths, income in retirement can come from multiple sources, some which are taxable and some which are not; planning where and how your income is generated with an eye toward taxes can have a significant impact on your finances in retirement.

In addition, planning can also include Roth conversions, QCD donations to charities, using HSA funds, as well as gifting to children or other beneficiaries. Gifting is one way to avoid capital gains on appreciated investments, as the tax burden from a realized capital gain is shifted to the beneficiary when they sell the investments.

Last but not least, based upon the total tax estimate, the Smiths need to make sure they are paying at least 90% of the total tax due or $21,222. Alternatively, there is a penalty proof withholding amount that can be calculated based on the previous year’s total tax and Adjusted Gross Income.

Please share with us your tax planning questions! We look forward to hearing from you.

share this post

share on facebook

email to a friend

pin to pinterest